Archive for the ‘3b. Economic Realities’ Category

Seth Godin: on being remarkable, the way to go viral

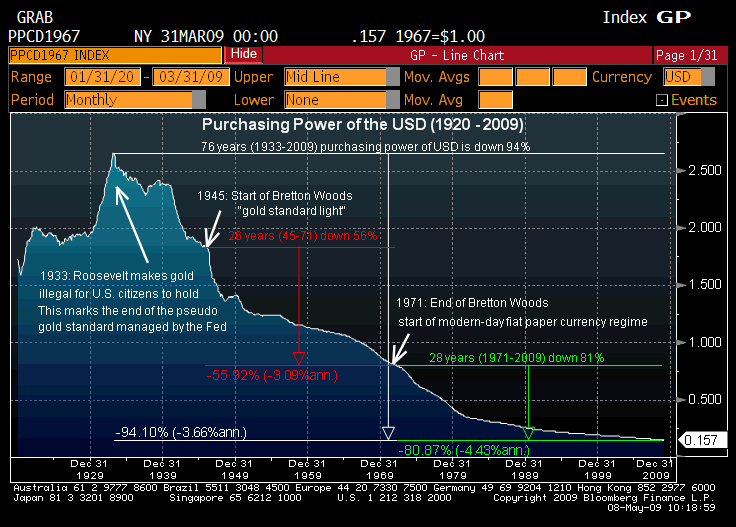

June 2, 2009Dollar’s Purchasing Power Annihilated – The Chart They Don’t Want You to See

May 19, 2009This is the chart they don’t want you to see: the purchasing power of the dollar over the past 76 years has declined by 94%. And based on current monetary and fiscal policy, we have at least another 94% to go. The only question is whether this will be achieved in 76 months this time.

Bank Lending Keeps Dropping

April 21, 2009Analysis of Treasury Data Paints Starker Picture Than Official Government Snapshots.

The Wall St. Journal

April 20, 2009

Lending at the biggest U.S. banks has fallen more sharply than realized, despite government efforts to pump billions of dollars into the financial sector.

Most bailed out Banks have reduced lending since getting funds. Unfortunately, one must subscribe to the Newspaper to get the full story. At least this is being reported in the Mainstream Media (MSM)

JGrace

Wage Deflation Sets In

March 26, 2009FED planning 15 fold increase in US Monetary Base

March 26, 2009http://www.marketskeptics.com/2009/03/fed-is-planning-15-fold-increase-in-us.html

by Eric deCarbonnel

The fed is planning moves that would more than double its balance-sheet assets by September to $4.5 trillion from $1.9 trillion. Whether expressing approval or concern over the fed’s intentions, most commentators fail to understand the real magnitude of the projected expansion of the US monetary base because they don’t take into account the amount of dollars circulating abroad.

At least 70 percent of all US currency is held outside the country, and this means the US monetary base is considerably smaller than the fed’s overall balance sheet. Take, for example, the true US domestic money supply at the beginning of September 2008, before the fed started its quantitative easing. From the Federal Reserve’s website, we know that currency in circulation was 833 Billion. This translates as 583 Billion dollars circulating abroad (70 percent), and 250 Billion dollars circulating domestically (30 percent). Since the bank reserve balances held with Federal Reserve Banks were 12 billion, that gives us a 262 Billion domestic monetary base as of September 2008. Now compare that to the projected US domestic monetary base for September 2009 which is 3,818 billion (4,500 billion – 583 billion (dollars circulating abroad) – 99 billion (other fed liabilities not part of the money supply)). The fed’s planned balance sheet expansion results in a 15-fold increase in the base money supply.

262 Billion = US monetary base as of September 2008 (minus dollars held abroad)

3,818 Billion = projected US monetary base in September 2009 (minus dollars held abroad)

3,818 Billion / 262 Billion = 15-Fold Increase in US monetary base

This is a staggering devaluation of the US currency! It means that for every dollar in America in September 2008, the fed is going to create fourteen more of them! Below is a rough sketch of what this increase in US monetary base would look like:

This 15-Fold Increase will be impossible to reverse

Next September, when the fed realizes it has gone too far and tries to reverse its balance sheet expansion, it will be unable to do so. The realities which will hinder the fed’s control of the money supply are:

1) The toxic assets filling its balance sheet

Expanding the money supply is easy. All the fed has to do is print dollars and then use them to buy assets. There is no effective limit to how much the fed can print and spend.

Shrinking the money is much trickier. To shrink the base money supply, the fed sell assets and takes the dollars it receives for them out of circulation. The amount the fed can shrink the money supply is therefore effectively limited by the market value of assets on its balance sheets. Since the fed is in the process of loading up on toxic securities while trying to restore health to the financial sector, it is now sitting billions of unrealized losses. These unrealized losses means the fed has little ammunition available to bring the money supply under control.

Once September rolls around, If the fed wants to reverse the expansion of its balance sheet and shrink the monetary base back down from 3,818 billion to 262 billion, then it will need to sell 3,556 billion worth of assets. However, the market value of its assets will only be worth a fraction of that.

2) Political constrains on fed’s actions

Even if the fed does try to shrink the money, it is likely to run into political constrains on its actions:

A) Selling toxic assets at a loss could become a crippling source of major embarrassment for the fed, undermining its authority. For example, last year when the fed took 29 billion toxic assets to help JPMorgan’s takeover of Bear Stearns, it assured Americans that by holding those securities till maturity, the cost to taxpayers would be minimal. If the fed sells those toxic Bearn Stearns assets at a catastrophic loss, it would cause fury and outrage from voters and lawmakers.

B) Selling assets at below book value will quickly cause the fed’s equity to turn negative. The Federal Reserve would then need to be recapitalized by new debt from the treasury, which would increase the national debt.

3) The benefits from of its balance sheet expansion would be lost if the fed starts selling assets

The fed is accumulating toxic mortgage backed securities, long term treasuries, and other assets to unfreeze the credit markets and spur economic growth. Turning around and selling those assets would result in the collapse of the credit markets and the financial system, which the fed has been desperately trying to prevent.

Upwards pressure on interest rates

On top of all the issues above, the fed’s woes are going to be compounded by upwards pressure on the yields of treasuries and other US debt. This upwards pressure will likely force the fed to monetize far more treasuries than the planned $300 billion purchases it has already announced, and will greatly complicate any efforts by the fed to control the money supply.

Below are the nine factors which will cause yields to move higher.